How I Navigated Kindergarten Costs Without Losing My Mind

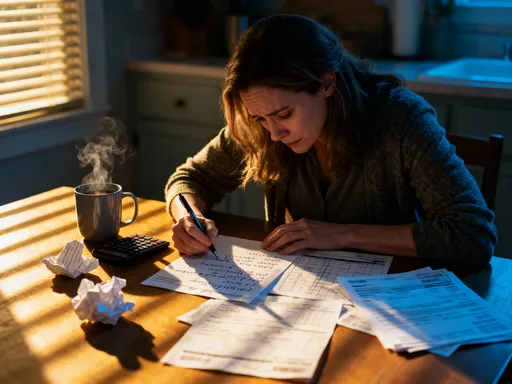

Paying for kindergarten hit me harder than I expected. It wasn’t just tuition—there were supplies, activities, and surprise fees that added up fast. I felt overwhelmed, like I was making financial decisions in the dark. That’s when I realized I needed a real plan, not just budgeting, but a clear way to assess risks and protect my family’s stability. This is how I found a smarter path—one that balances cost, quality, and peace of mind. What started as a stressful scramble became a turning point in how I manage our household finances. I learned that early education isn’t just about a child’s development; it’s also a financial milestone that demands attention, strategy, and foresight.

The Shock of Hidden Education Costs

Many parents enter kindergarten season believing it will be simple and low-cost, only to be blindsided by expenses that accumulate beyond the initial tuition quote. While public schools often advertise free enrollment, the reality includes a cascade of additional costs that are rarely highlighted upfront. These can include classroom supplies, field trip fees, technology charges for tablets or learning apps, special event tickets, school uniforms, transportation if outside the zone, and even contributions to class funds that, while technically optional, feel socially expected. A backpack that costs $40, a tablet rental of $75 per year, or a single field trip priced at $25 may seem minor in isolation. But when combined with other recurring fees, they can total several hundred dollars annually—sometimes more than a monthly mortgage payment for some families.

The emotional weight of these hidden costs often hits hardest because they arrive without warning. A parent might budget carefully for the fall semester, only to receive an email in October requesting $30 for an art festival or $50 for a winter performance costume. These surprise charges disrupt cash flow and force last-minute financial decisions, often leading to credit card use or dipping into emergency savings. The stress is compounded by the pressure to provide equally for every child, especially in households with multiple kids in different grades. Over time, these small, unplanned expenses erode financial confidence and can create a sense of failure, even when the household is otherwise managing well. The truth is, no parent wants to say no to their child’s school experience, but consistently saying yes without planning can lead to long-term strain.

Understanding the full scope of kindergarten-related spending begins with acknowledging that education today is rarely free, even when labeled as such. The modern classroom operates with expectations that go beyond textbooks and pencils. Schools may require specific brands of supplies, digital devices, or participation in enrichment programs that carry fees. Some institutions even charge for extended-day care or early drop-off, which can be essential for working parents. Recognizing these hidden layers is the first step toward financial preparedness. It shifts the mindset from reacting to each new request to anticipating and preparing for them in advance. When parents treat kindergarten as a financial commitment with predictable and unpredictable elements, they are better equipped to handle the full cost picture without guilt or panic.

Why Risk Assessment Matters in Early Education Spending

When it comes to children, spending feels urgent and deeply emotional. Saying yes to a school request often feels like supporting your child’s growth, while hesitation can feel like withholding opportunity. Yet, treating education expenses like impulsive purchases rather than deliberate financial decisions can lead to serious long-term consequences. This is where risk assessment becomes essential. In simple terms, risk assessment means evaluating what you can afford today against what you might need tomorrow. It involves asking not just “Can I pay this now?” but “What happens if I keep paying things like this over time?” For families, especially those with limited income flexibility, overcommitting at the kindergarten level can jeopardize bigger goals like homeownership, retirement savings, or future college funds.

Consider two families facing the same $60 after-school enrichment program. Family A pays without hesitation, using a credit card to cover the cost, assuming it’s a one-time expense. But when similar fees arise for music lessons, holiday parties, and science fairs, their card balance grows. Over a year, those small yeses add up to over $1,000 in debt, accruing interest and creating ongoing monthly payments. Family B, however, pauses. They assess their current budget, consider the value of the program, and decide to enroll only if they can pay in full without strain. They might choose a free community alternative or wait for a scholarship spot. Their decision isn’t about denying their child opportunity—it’s about protecting the household’s financial health.

Risk assessment also involves understanding opportunity cost—the value of what you give up when you choose one path over another. Every dollar spent on non-essential school fees is a dollar not saved for a rainy day or invested in long-term security. By applying a disciplined evaluation process, parents can avoid the trap of emotional spending and instead make choices aligned with both their child’s needs and their family’s future. This doesn’t mean cutting corners on education quality. It means being intentional. It means recognizing that financial stability is itself a form of care. When parents assess risks before spending, they model responsibility, reduce anxiety, and create space for more meaningful financial decisions down the road.

Mapping Your Financial Exposure

Before writing a single check or approving a school fee, it’s crucial to map out your full financial exposure. This means creating a comprehensive list of every possible kindergarten-related expense, not just the ones listed in the enrollment packet. Start with the obvious: tuition (if applicable), registration fees, and mandatory supplies. Then expand to recurring costs like monthly lunch payments, transportation fees, or after-school care. Don’t overlook seasonal expenses—back-to-school shopping, holiday events, end-of-year parties, or summer bridge programs. Even small annual fees, like a $15 class photo or $20 for a school T-shirt, should be included because they contribute to the total burden.

To build an accurate map, gather information from multiple sources. Review past school invoices, talk to other parents, and request a full fee schedule from the school administration. Many institutions provide itemized lists upon request, even if they aren’t advertised. Once you have a list, categorize each expense as essential, optional, or flexible. Essential costs are those required for enrollment and daily participation—basic supplies, transportation if no alternative exists, or mandatory technology fees. Optional expenses include things like extracurricular clubs, special events, or premium enrichment programs. Flexible costs are those you can control through timing or choice—buying supplies in bulk, using hand-me-downs, or selecting lower-cost alternatives.

Next, assign realistic dollar amounts and frequencies. A $30 field trip may occur four times a year, totaling $120. Lunch at $4 per day adds up to $80 weekly, or about $1,400 annually for a full school year. After-school care at $150 per week becomes a $600 monthly expense. When these figures are totaled, the true cost of kindergarten often exceeds initial expectations. But this clarity is empowering. It allows families to adjust their budgets proactively, set aside money monthly, or identify areas where savings are possible. Some parents find it helpful to create a dedicated “education fund” in their banking app, automatically transferring a set amount each payday. This method turns a large, intimidating cost into manageable, predictable installments. By mapping exposure, families move from fear to control, from surprise to strategy.

Comparing School Options with Financial Realism

Choosing a kindergarten is one of the first major decisions parents make for their child’s future, but it should also be one of the most financially informed. Public, private, charter, and religious schools each come with distinct cost structures and long-term financial implications. Public schools typically have no tuition, but they may still require families to cover supplies, activity fees, and transportation if living outside the district. Charter schools, while publicly funded, sometimes request voluntary donations or charge for extended-day programs. Private schools often carry high tuition—ranging from a few thousand to over $20,000 annually—but may offer more resources, smaller class sizes, or specialized curricula. Religious schools might offer lower tuition in exchange for church membership or volunteer hours.

The sticker price is only part of the story. Families must also consider indirect costs. For example, a private school with excellent academics might be located 30 minutes from home, requiring daily gas, parking, or paid drop-off services. If both parents work, the time and cost of transportation could outweigh the educational benefits. Similarly, a school without on-site after-school care may force parents to pay for external programs, adding hundreds per month to the total expense. Location, schedule flexibility, and support services all influence the real cost of attendance. A school that offers free early drop-off or subsidized lunch programs can provide significant financial relief, even if the base fees are slightly higher.

When comparing options, parents should evaluate value, not just cost. Value includes transparency in billing, availability of financial aid, and the school’s track record in supporting student success. Some institutions publish full cost breakdowns or offer payment plans, which can ease cash flow. Others may have strong parent communities that organize supply swaps or fundraising to reduce individual burdens. Visiting schools, asking detailed questions, and speaking with current families can reveal hidden financial trade-offs. The goal is not to choose the cheapest option, but the one that aligns best with both educational goals and financial reality. A balanced decision considers not just what you pay now, but how it affects your household’s stability for years to come.

Building a Safety Net Around Education Costs

No matter how carefully you plan, unexpected expenses will arise. A teacher might introduce a new science kit mid-year, a school event could require last-minute travel, or a family’s income might temporarily decrease due to reduced hours or medical leave. This is why risk control is just as important as budgeting. A financial safety net acts as a buffer, protecting your household from being derailed by unforeseen education costs. The most effective way to build this protection is through dedicated savings. Even setting aside $25 or $50 per month in a separate account can create a cushion of several hundred dollars by the time surprise fees appear.

Some families use flexible savings accounts or high-yield savings accounts specifically labeled for education. These accounts keep the money accessible but separate from everyday spending, reducing the temptation to use it for non-essential purchases. Automatic transfers ensure consistency, turning saving into a habit rather than a chore. For households with variable incomes, such as freelancers or part-time workers, seasonal budgeting can help. This involves saving more during high-earning months to cover expenses during leaner periods, including back-to-school season. By aligning savings with income cycles, families maintain stability without overextending.

Another key strategy is to build in financial flexibility. This means avoiding long-term commitments that lock in high payments without escape clauses. For example, signing a full-year contract for after-school care might seem convenient, but it leaves little room to adjust if needs or income change. Month-to-month options, while sometimes slightly more expensive, offer greater control. Similarly, choosing schools with transparent refund policies or sliding-scale fees can provide peace of mind. The goal is not to eliminate all risk—this is impossible—but to reduce its impact. When families prepare for the unexpected, they gain confidence. They know they can handle surprises without panic, debt, or guilt. That confidence, in turn, strengthens their overall financial well-being.

Smart Trade-Offs That Don’t Sacrifice Quality

One of the greatest misconceptions about financial discipline is that it requires sacrificing quality. In reality, smart trade-offs can preserve educational value while significantly reducing costs. The key is intentionality—making conscious choices based on priorities rather than impulses. For example, buying gently used school supplies from community swap events or online parent groups can cut supply costs by 50% or more. Many schools even host annual “supply drives” where families donate leftover items, which are then redistributed for free. Textbooks, backpacks, lunchboxes, and uniforms often remain in excellent condition after one year and can be passed down or purchased secondhand at a fraction of retail prices.

Timing also plays a crucial role in savings. Purchasing supplies during late-summer sales, using cashback apps, or waiting for school-specific discount events can lead to major reductions. Some retailers offer early-payment discounts for tuition or activity fees—paying in full by a certain date might save 5% or more. Families who plan ahead and monitor these opportunities can redirect hundreds of dollars back into their budgets. Another effective strategy is pooling resources with other parents. A group might collectively buy classroom materials in bulk, splitting the cost and reducing individual expenses. Shared transportation schedules can also cut gas and time costs, especially for field trips or after-school activities.

Choosing a mid-tier private school instead of the most expensive option can also offer strong academics without the premium price tag. Similarly, enrolling in a high-performing public or charter school with strong community support can provide excellent education at little to no cost. The focus should be on outcomes—does the school help children develop literacy, social skills, and confidence?—rather than prestige or amenities. By prioritizing what truly matters, families can make choices that honor both their values and their financial limits. These trade-offs aren’t about deprivation; they’re about empowerment. They demonstrate that responsible financial behavior and high-quality education can coexist.

Long-Term Gains from Early Financial Discipline

The decisions made during the kindergarten years do more than cover a single school year—they shape a family’s financial culture for decades. When parents approach education spending with discipline, clarity, and risk awareness, they set a foundation for future success. The habits formed early—tracking expenses, saving in advance, evaluating value—become automatic over time. These practices don’t disappear after kindergarten; they carry forward into elementary, middle, and high school, where costs only increase. Families who master financial planning early are better prepared for college savings, car purchases, home upgrades, and retirement.

Moreover, this discipline reduces anxiety. Financial stress is a major burden for parents, especially women who often manage household budgets. Knowing that you have a plan, a safety net, and a clear understanding of your obligations brings peace of mind. It allows parents to engage with their child’s education from a place of presence, not panic. They can celebrate achievements, support learning, and participate in school life without the constant background worry of money. This emotional relief is a powerful benefit—one that improves family relationships and personal well-being.

Finally, early financial discipline teaches children valuable lessons by example. When kids see their parents making thoughtful choices, budgeting wisely, and planning for the future, they absorb those behaviors. They learn that money is not something to fear or ignore, but a tool to be managed with care. These lessons become part of their own financial identity, setting them up for responsible adulthood. In this way, navigating kindergarten costs is not just about surviving one year of expenses. It’s about building a legacy of stability, resilience, and confidence. By treating early education as a financial milestone, families gain more than savings—they gain control, clarity, and the freedom to focus on what truly matters: their child’s growth and their own peace of mind.